As sales double in Q2 2025

Electric vehicle sales across Southeast Asia more than doubled in the second quarter of 2025, driven by rapid growth from Chinese and Vietnamese automakers, as well as a shift in regional consumer demand towards lower-emission transport.

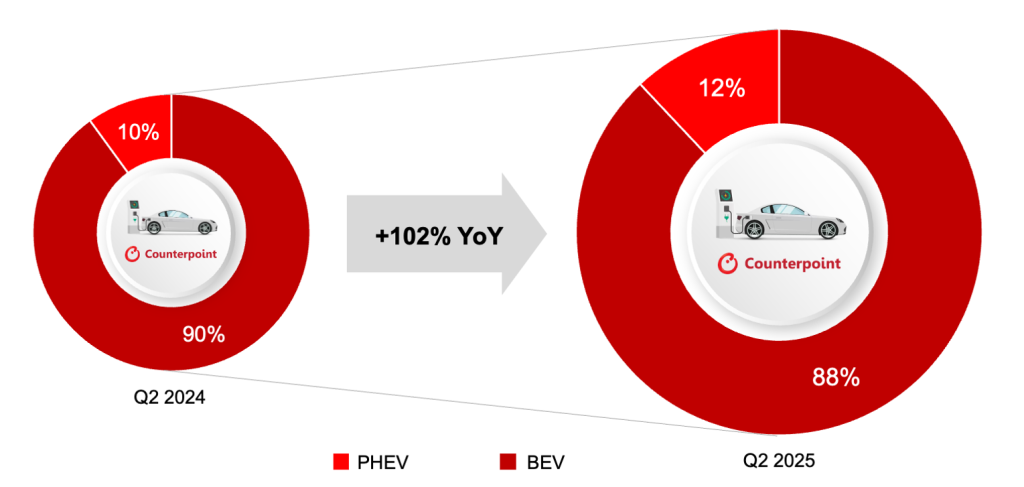

According to data from Counterpoint Research, electric vehicle (EV) sales — including both battery electric vehicles (BEVs) and plug-in hybrids (PHEVs) — increased 102% year-on-year in Q2, making it one of the fastest adoption rates worldwide.

The region’s accelerating transition toward electrification reflects increasing affordability, improved awareness, and new production capacity from regional and Chinese players.

BEVs continued to be the primary driver of this growth, with sales increasing by 99% from the previous year. Plug-in hybrids, which account for just 12% of total EV sales, gained traction as buyers sought flexibility amid ongoing charging infrastructure gaps in several Southeast Asian markets. Although still below the global average PHEV share of 34%, the segment is steadily expanding across the region.

Market shifts

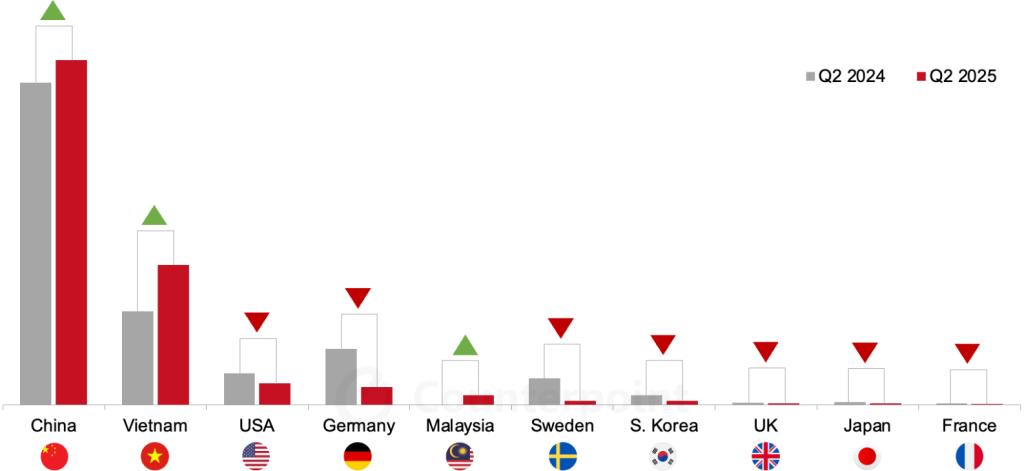

Chinese-origin carmakers captured a 63% share of the Southeast Asian EV market in Q2 2025, up from 53% a year earlier. BYD, the world’s leading EV manufacturer by sales volume, expanded its presence with aggressive pricing and a wide model range tailored to regional needs.

Vietnam’s VinFast also strengthened its position, accounting for more than 25% of all EVs sold in Southeast Asia during the quarter.

Malaysia marked a significant development with Proton launching its e.MAS brand, the country’s first serious EV effort. Backed by national industrial policy and increasing local production, Proton’s entry highlights a broader push across ASEAN to reduce dependence on fossil fuels while developing domestic EV ecosystems.

Vietnam and Malaysia’s growing presence in the EV market also reflects deeper government support and industrial strategies aimed at reducing imports and increasing local manufacturing.

In particular, Vietnam’s EV market is benefiting from targeted investment and increased production capacity. At the same time, Malaysia’s government has offered tax exemptions and infrastructure support to attract EV manufacturers and boost domestic assembly.

Lagging rivals

In contrast, legacy automakers from Japan, South Korea, the US, and Europe continued to struggle to gain traction in Southeast Asia’s rapidly evolving EV market. These brands have been slower to roll out competitive EV portfolios in the region and remain reliant on traditional internal combustion engines or conventional hybrids.

“Japanese and South Korean OEMs, such as Toyota, Honda, Nissan and Hyundai-Kia, face challenges stemming from slower EV portfolio rollouts, continued reliance on hybrids, and limited local assembly presence compared with their Chinese peers, leaving them unable to compete effectively in SEA’s fast-growing EV landscape,” said Liz Lee, Associate Director at Counterpoint.

While Hyundai-Kia has made progress in some Southeast Asian markets, such as Indonesia, it has yet to scale in others, where Chinese and regional brands are outpacing it in terms of affordability, localisation, and supply chain agility.

Future outlook

With global automakers facing pressure to electrify, Southeast Asia is emerging as a key battleground for the automotive industry. Although EV penetration in the region remains lower than in Europe or China, the Q2 data highlights how quickly the landscape is shifting — and how structural advantages, such as local assembly and price competitiveness, are reshaping the market in favour of Chinese and regional brands.

According to the International Energy Agency (IEA), global EV sales are expected to reach 17 million units in 2025, up from 14 million in 2024. While China remains the largest market globally, Southeast Asia’s trajectory is increasingly significant, particularly as governments in countries like Thailand, Indonesia, and Vietnam continue to roll out EV incentives and infrastructure investments.

If current trends persist, local brands such as VinFast and Proton could further consolidate their market positions, potentially reshaping Southeast Asia’s automotive supply chains and regional trade dynamics.

For Middle East stakeholders observing the evolution of EV adoption, the Southeast Asian experience provides a glimpse into how industrial policy, pricing strategies, and infrastructure gaps intersect to drive or delay the transition.

Searches related to “EV sales in Asia,” “BYD market share,” and “VinFast expansion” have trended across platforms in 2025, underscoring investor and consumer interest in how new players are disrupting established markets.

Image: BYD has expanded its presence in SEA with aggressive pricing and a wide range of models tailored to regional needs. Credit: BYD