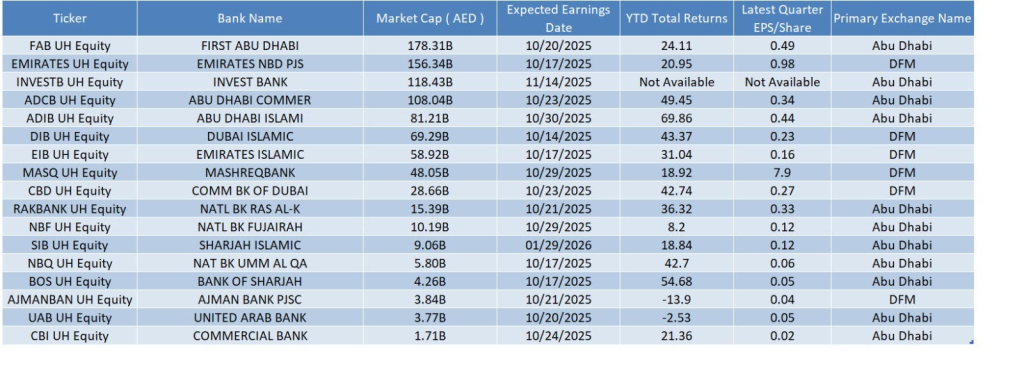

UAE bank earnings are about to kick start, with prominent names, Emirates NBD and Dubai Islamic Bank, scheduled to announce their Q3 earnings this week. The earnings will serve as a bellwether event for the market, dictating the overall tone and momentum of future DFM and ADX index price movements. Much has been talked about the ongoing rapid rise in real estate prices, especially in the UAE and Dubai. As such, each bank’s own market projections and provisioning requirements will serve as an indirect indicator of the state of the current UAE economy and its key sectors, like real estate and retail trade.

Below, we look at key trends and narratives to watch out for –

A) Lending Growth Needs To Ride Higher As Margin Compression Fears Dominate

For top UAE banks, markets have estimated a bare minimum required loan growth rate of 10 % to sustain the current revenue expansion trend. This is especially necessary in times when overall margin compression is likely for UAE banks. The overall dovish interest rate trajectory implies similar changes in local UAE lending rates as the dirham is pegged against the dollar. For major UAE banks, for H1, the overall lending growth rate was 8%, primarily aided by the wholesale segments’ 9% growth rate. While the overall 18% retail growth continues to support the lending growth trajectory here, the increasing consensus of wholesale segment lending growing by 13% over 25–26 could provide more impetus to the overall credit markets. UAE’s project pipeline of nearly $450 billion over the next 5 years could see almost 40% to 50% loan account utilization, supporting the overall uptick in wholesale loan growth.

B) Non-Interest Income and Other Income Yet Again Likely To Be Key

For UAE banks, non-interest income now accounts for nearly 40% of the total operating revenue, marking a sizable growth over the previous year and reaching its 2021 highs at 46.5%. For this segment, notable peaks were observed during 2005 and 2021, with highs seen in the 52% to 54% range in the 2005 – 2009 cycle. Some of the primary reasons for the ongoing rapid rise in non-interest income include banks’ increasing reliance on digital transformation strategies, sovereign diversification initiatives, and the overall rise in expat residency population in key hubs like Dubai and Abu Dhabi.

C) Cost of Funding Optimization

Despite a 19 bps fall in the three-month interest rate during the last quarter, UAE banks saw a median increase of 10 bps in interest-bearing deposits. This was primarily driven by the higher cost of interest-bearing liabilities and the overall market demand in the mix of bank deposit products, which tilted towards costlier and higher-yielding options. For investors, a specific concern would be the impact of a fall in interest rates from late Q4’25 – Q1’26 onwards on the UAE banks’ margin. For UAE banks, Q3 could still see margin holding up as banks gear up towards the Fed’s aggressive rate cut cycle from 2026.

Source: Central Bank of UAE Financial Stability Report 2024 & 2025, MEED Data Publication, Bloomberg EQS, RV, BI Functions