Last week was the moment global markets stopped treating strong data as good news. The catalyst was Friday’s May US payrolls, which rose by 172,000 versus expectations of 80,000. US unemployment held at 4.3%, and prior months were revised up by 93,000. This left the US Federal Reserve with less room to lean dovish and gave rates markets permission to price a policy path which could see a rate increase this year. The 2-year Treasury yield rose to a 15-month high of 4.147%, the 10-year pushed toward 4.54%, and the dollar strengthened as the market moved back toward higher-for-longer.

Equities took the hit where positioning was most crowded. The S&P 500 fell 2.64% on Friday, ending a nine-week winning streak, while the Nasdaq dropped 4.18%. The real damage was in the AI complex. The Philadelphia Semiconductor Index fell 10.3%, its worst day since March 2020, with US-listed chipmakers losing around $1.3 trillion in market value.

The stress was cross-asset rather than equity-specific. Brent crude oil still finished the week supported near $93 as Middle East risk kept an inflation premium in energy. Gold fell more than 3% as higher real yields and a firmer dollar overpowered safe-haven demand. Crypto was weaker still, with Bitcoin down nearly 18% on the week.

Risk appetite for the coming week will be tested by US Consumer Price Index (CPI) inflation data on Wednesday and the European Central Bank (ECB) meeting on Thursday.

A Bruised Bitcoin Enters CPI Week

Bitcoin’s managed to tread water just above $60k over the weekend, but still enters the week bruised from the selloff earlier last week. The token fell over 15% on the week, briefly trading below $60k, touching an intraday low near $59,100, and hitting its weakest level since October 2024. The move lower was certainly exacerbated by the strong US payrolls report from Friday, but there were notable other catalysts from earlier in the week.

Michael Saylor’s Strategy sold 32 Bitcoin, worth around $2.5 million, tiny compared with its 843,706 Bitcoin holdings, but important because it challenged the sector’s permanent buyer narrative.

US spot Bitcoin ETFs have now endured a 13-session redemption streak that drained roughly $4.4 billion from the category, cutting ETF assets from about $104 billion to $80 billion since mid-May.

Given the hit to sentiment over the past week, the coming days are key for the cryptocurrency. Bitcoin needs ETF flows to stabilise and macro data to stop pushing yields higher. If US CPI inflation (covered below) reinforces the higher-for-longer narrative, the coin could come under further pressure.

CPI Takes The Wheel

The May US CPI print lands on Wednesday with markets already in a less forgiving mood. The inflation backdrop is already awkward. April CPI rose 0.6% month-on-month MoM after a 0.9% gain in March, lifting headline inflation to 3.8% year-on-year (YoY) from 3.3%. Core CPI rose, with energy the clear accelerant.

Consensus for May is for a further increase in headline CPI 0.5% MoM and 4.2% YoY, which would be the highest inflation rate in three years. Core is expected to rise 0.3% MoM and 2.9% YoY. The key market issue is whether this remains an energy-led spike or starts to bleed into core services and goods. A firm core print would likely worry traders more than just a hot headline figure, and could potentially keep pressure on multiple assets heading into the June FOMC meeting next week.

The ECB Get Set To Hike

The latest Reuters economist survey shows more than 90% expect the ECB to raise the deposit rate by 0.25% when the central bank meets on Thursday.

The case for tightening is based predominantly on concern around higher inflation. Eurozone headline inflation rose to 3.2% in May from 3.0% in April and 2.6% in March, leaving the rate well above the 2% target. Energy inflation remains the main driver, running at 10.9% year-on-year, but the more uncomfortable detail is that services inflation accelerated to 3.5% from 3.0%, while non-energy industrial goods inflation edged up to 0.9%.

The problem is that the growth side of the ECB’s mandate is also deteriorating. Euro area GDP grew just 0.1% quarter-on-quarter (QoQ) in Q1, employment growth slowed to 0.1%, and the composite PMI slipped to 48.5 in May, signalling contraction. Manufacturing PMI fell to 51.6 from 52.2, while input costs rose at the fastest pace in four years.

Even though the hike is mostly factored in by the currency and bond markets, the bigger question is whether President Lagarde validates a full hiking cycle. With inflation sticky but activity weakening, traders will be watching for signs that further hikes might be needed later this year and what conditions would be needed to justify such a move.

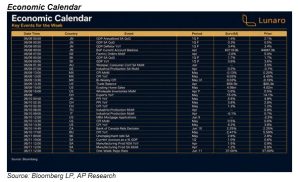

Economic Calendar

Source: Bloomberg LP, AP Research

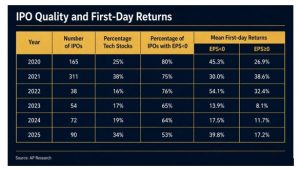

Chart of the Week

SpaceX is set to go public on Friday, June 12th, marking one of the hottest IPOs in several years. Despite some concerns about the earnings per share (EPS), data shows that the mean first trading day returns for loss-making companies don’t have to be negative: